Welcome to the 8th edition of Signature Block, a newsletter for emerging fund managers. If someone forwarded this to you, subscribe here to get the next one in your inbox.

We don’t live in a normal world in venture. We live in a world ruled by the power law.

<insert dramatic orchestral music>

Passing on startups that go on to become breakout companies can result in multi-million dollar mistakes. The biggest mistakes in venture are “errors of omission” not “errors of commission.”

Hindsight of course is 20/20. Looking back at passes, it’s obvious how we could’ve made better decisions. Signals that feel obvious looking back weren’t obvious at the outset. Also, reasons for passing on investments vary, and every investor, company and deal is unique.

Yet, there are patterns across big misses and lessons to be learned that can make you a better investor. In this edition of Signature Block, you’ll hear investors share (perhaps painfully) their biggest misses, why they passed, and lessons learned. We’ve also included some lessons from public “anti-portfolios” like Bessemer’s Anti-Portfolio.

Shout out to AJ Solimine for suggesting this topic.

Here are four main takeaways from this edition:

Have an open mind. While there are many patterns across successful startups, there is no formula that can predict startup success. This is one of the central paradoxes of our jobs. Innovation often looks strange, feels novel, and doesn’t pattern match well.

Ask yourself “why will this work?” Some of the biggest passes were a result of investors asking themselves “why won’t this work?” when they should have been asking “why will this work?” Counter-intuitively, the more knowledgeable you are about a space, the fewer the unknown unknowns and easier it is to come up with reasons why something won’t work. Of course, we aren’t celebrating naiveté but instead highlighting potential blind spots that can drive an investor to pass on promising opportunities.

Also ask “if this works, what can this become?” The biggest technology companies “earn the right” to solve more of their customers’ problems and unlock new markets over time. Some big passes we came across were a result of investors’ inability to see (1) how a company could grow a market (Uber being a classic example) and (2) the second-order markets a company could unlock over time. This is particularly hard because it requires second-order thinking.

Entry valuations are “relative” to return potential. While it’s important that entry valuations for your portfolio align with your fund strategy, investing in companies at premium valuations can still drive fund-returning outcomes. Some of the biggest misses investors had were a result of passing on companies that seemed too “expensive”, too “rich”, or too “hyped”.

It’s worth noting that anyone who’s been investing for a substantial amount of time – including the world’s best investors – has big misses. As an investor, you should be concerned if you haven’t had an opportunity to make the mistake of passing on a generational company. We’ll share more thoughts on how to improve deal flow in a future edition of Signature Block. :)

Nicholas Chirls @ Notation Capital’s Big Miss in Headway

Nicholas from Notional Capital passed on Headway’s pre-seed round. The company is now valued at $750M. One of his learnings was to maintain an open mind, even in well-traversed and highly-competitive spaces, and look for insights that the company has that could give them an unfair advantage.

Here’s more from Nicholas directly:

A pass that really hurts for me is Headway, a mental health marketplace and provider network. We passed on the pre-seed round and I think about it all the time because the company has the potential to be a category-defining company in NYC. Their most recent round raised $75M led by a16z.

I passed at the time mainly because there were a few similar mental health provider search products in the market, and I wrongly bucketed them in the same camp. Instead, they eventually chose to build out a provider network to help providers manage insurance payments, which proved to be a much better model, both for patients to find in-network care, and a much better business for Headway. My main learning here is to always find ways to keep an open mind, even in what are seemingly competitive spaces and look for innovative approaches and business models that can stand out above the rest, particularly in this case because I had already dug into the category more broadly and wanted to make a mental health investment at the time. Doh!

AJ Solimine + Evan Tana @ Script Capital’s Big Miss in Meesho

Early in their fund, AJ and Evan passed on Meesho which today would have delivered a ~500x return on capital. Their decision was driven by the company’s tight runway and fear of losing their investment. Loss aversion, which first-time fund managers are especially susceptible to, can make you more focused on avoiding losses more so than making gains. In reality, you can only lose 1x your money but the best investments can deliver 100x+ multiples.

Here’s more from AJ and Evan:

Evan and I have been interested in WhatsApp as a general commerce platform for about as long as we can remember. So in early 2017 when a friend sent us the concept for Meesho, a social selling platform in India - we jumped at the opportunity to meet.

After chatting with Meesho’s CEO, Vidit, about the business and progress we were convinced there was a huge opportunity and Vidit was special, so we committed to invest.

We were a few months into fundraising for our first fund, and a big part of pitching LPs involves showing off the existing portfolio so new LPs know what they’re buying into. Meesho would be one of our first 3 investments out of the fund.

Naturally, we were concerned about runway to ensure we wouldn’t have to pitch LPs with any shutdowns already in our portfolio. So before closing the investment, we asked Meesho for recent financials and marketing spend and realized that with their current spend, they were running on a very tight runway. We got spooked. We told Vidit that based on the limited runway, we couldn’t get comfortable making the investment.

On a micro level - it made sense to avoid potential shutdowns in the portfolio while the fund was getting off the ground and we were still pitching LPs. But that conservative strategy led us to miss an investment that could ~500x+ our original investment (Meesho recently raised at a $5B valuation).

I think as young VCs we often suffered from Loss Aversion - we experienced this again with some crypto investments we missed in 2017-18 (including the Polygon, fka Matic, seed round). We were so afraid of a quick potential shutdown that we missed what we knew could be a 1,000x return. Since then, we’ve learned how to calibrate our decisions and have a number of unicorns under our belt now. But missing Meesho (and Polygon) has definitely caused quite a lot of lost sleep over the years…

Elizabeth Yin’s Big Miss in Bitcoin

Elizabeth Yin learned about Bitcoin in 2011 but didn’t invest. Even a small investment of $1,000 at that time would have appreciated to $40,000,000 at today’s price.

The future is hard to predict. One way to hedge against that is through a portfolio strategy by placing several smaller bets on innovations that have the potential to have extreme outcomes (emphasis on “extreme”).

Here’s more from Elizabeth:

Honestly, my biggest miss was probably Bitcoin. I learned about it in early 2011 or so, and I think it was about 50 cents, maybe a little under that. More recently, even with the crash, Bitcoin is around $20,000 per Bitcoin, so that's a 40,000x miss.

Certainly I did buy a little bit a lot later, but have nowhere near those gains.

But in all seriousness, I think, you know, while this sounds laughable, I think that one of my biggest learnings is that sometimes it makes sense to just take a small flyer on many things. There are many investments that are accessible to the general public, including cryptocurrency, and you never really know where anything is going to go.

Ryan Hoover & Vedika Jain @ Weekend Fund’s Big Miss in Sorare

We passed on the seed round of two multi-billion dollar companies (so far!) at Weekend Fund.

Here’s the story of one: We passed on Sorare’s seed round in April 2020, shortly before the NFT boom. Only 18 months later the company raised another $680M valuing Sorare at $4.3B, a ~250x increase in valuation since our initial conversation.

Here’s more from us:

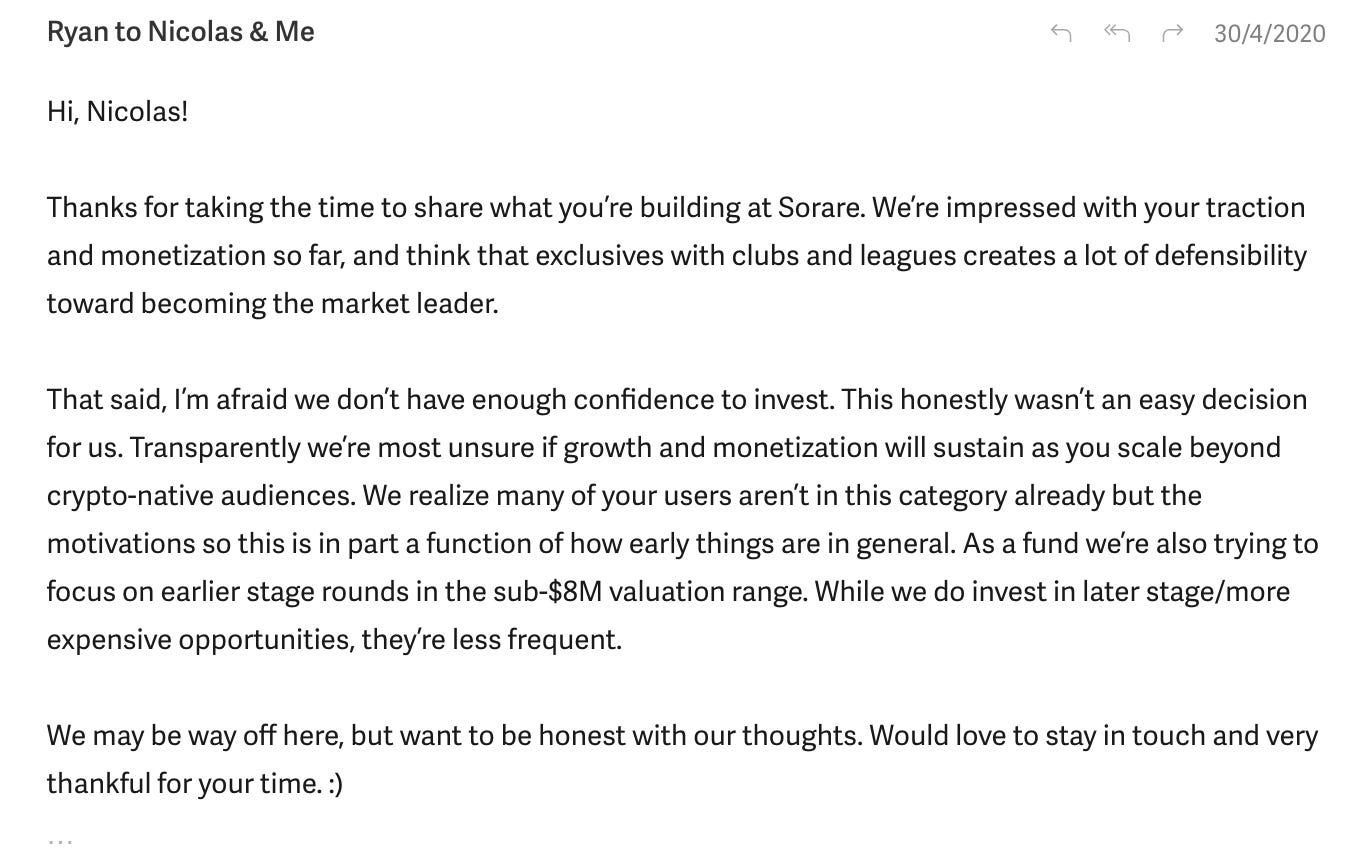

We were introduced to the company through, Kyran Schmidt, who was then at Seedcamp. In his email to us, he informed us that Sorare was “addicting half our team at Seedcamp(!)” and that they were raising a seed round.

We were extremely impressed with their traction – even though the football season was on pause – and the opportunity to sign exclusives with clubs, leagues, and other sports rights holders. They were well-positioned to create a moat within the space and become the market leader (the same way that FIFA soccer is the dominant soccer game in the video games world).

After a lot of back and forth, we ended up passing on the company driven by doubts about whether they’ll be able to sustain their growth as they scale beyond crypto-native audiences. Our intuition was that a large % of paying users were purely speculating and worried that it would be unsustainable. Combined with a higher valuation than we normally entered at the seed stage at that time, we opted to pass on the opportunity.

Here’s a screenshot of the email we sent Nicolas:

Some of our learnings:

We underestimated the value of a small but intense group of early adopters. We should have taken Kyran’s comment about his team members’ “addiction” more seriously. What people are procrastinating with holds some secrets about what is going to blow up.

We weighed too heavily the speculation in the game, and more generally, a reason for why Sorare won’t work rather than why it will work.

At the time, we weren’t actively pursuing NFT-driven businesses and lacked perspective on their potential.

Bessemer’s Big Miss in Airbnb, Apple, Atlassian, and More

Bessemer Ventures Anti-Portfolio shows that some of their biggest misses were a result of passing on companies that looked too expensive relative to other companies at similar stages in the market, but in hindsight, were extremely cheap relative to their return potential. While younger investors might be more susceptible to this, experienced investors aren’t immune to this either.

More from them:

Jeremy Levine met Brian Chesky in January 2010, the first $100K revenue month. Brian’s $40M valuation ask was “crazy,” but Jeremy was impressed and made a plan to reconnect in May. Unbeknownst to Jeremy, $100K in January became 200 in February and 300 in March. In April, Airbnb raised money at 1.5X the “crazy” price. Their last fundraising was completed at ~500X that valuation.

Bessemer had the opportunity to invest in pre-IPO secondary stock in Apple at a $60M valuation. Neill Brownstein called it “outrageously expensive.”

Byron Deeter flew straight to Atlassian in 2006 when he caught wind of a developer tool from Australia (of all places!). Notes from the meeting included “totally self-financed, started with a credit card” and “great business, but Scott & Mike don’t ever want to be a public company.” Years and countless meetings later, the first opportunity to invest emerged in 2010, but the $400M company valuation was thought to be a tad “rich.”

If you’re a new fund manager, thinking of starting a fund, or just curious, subscribe to Signature Block if you haven’t already. If you think this might be useful for emerging managers, share on Twitter.

Lastly, let us know what topic you’d like us to cover in the next edition.

Until next time, Ryan and Vedika from Weekend Fund :)